Buy the outcome, not the software

Seat-based software sells you access. AI agents sell the finished work, the service-as-software shift. Why the orchestrator now buys outcomes, not seats.

Salesforce turned software into a subscription in 2000 and set the template that held for a quarter century. You bought seats, your team logged in and the actual work still landed on someone in your building. You paid for access. You supplied the labor. That was the deal.

The deal you stopped noticing

Seat-based SaaS is a rental on access. Salesforce, Zendesk, the whole catalog: you rent the tool, then you hire and manage the humans who operate it. The vendor sells you a faster way to do the work. They never sell you the work.

That distinction sounds small. It is the whole game.

Sarah Tavel, a partner at Benchmark, put it plainly in August 2023: sell work, not software.1 Her argument was aimed at founders. Read it as a buyer and it reframes every line item you approve. When a vendor sells software, you are still on the hook for the result. When a vendor sells work, the result is theirs to deliver.

What the vendor now owns

a16z’s enterprise team said it in June 2025: AI software often “sells the work output itself, instead of selling software to help the people do the work.”2 Foundation Capital gave the shift a name, service as software, and a number: a 4.6 trillion dollar opportunity, because you are no longer competing for a software budget, you are competing for a payroll budget.3

Watch how the pricing tells on itself. Zendesk charges around 115 dollars per seat per month and trusts you to make the seats worth it. Intercom’s Fin agent charges 99 cents per resolved ticket.4 One is a login. The other is a closed ticket. As a buyer you can feel which you would rather pay for.

The market already re-priced it

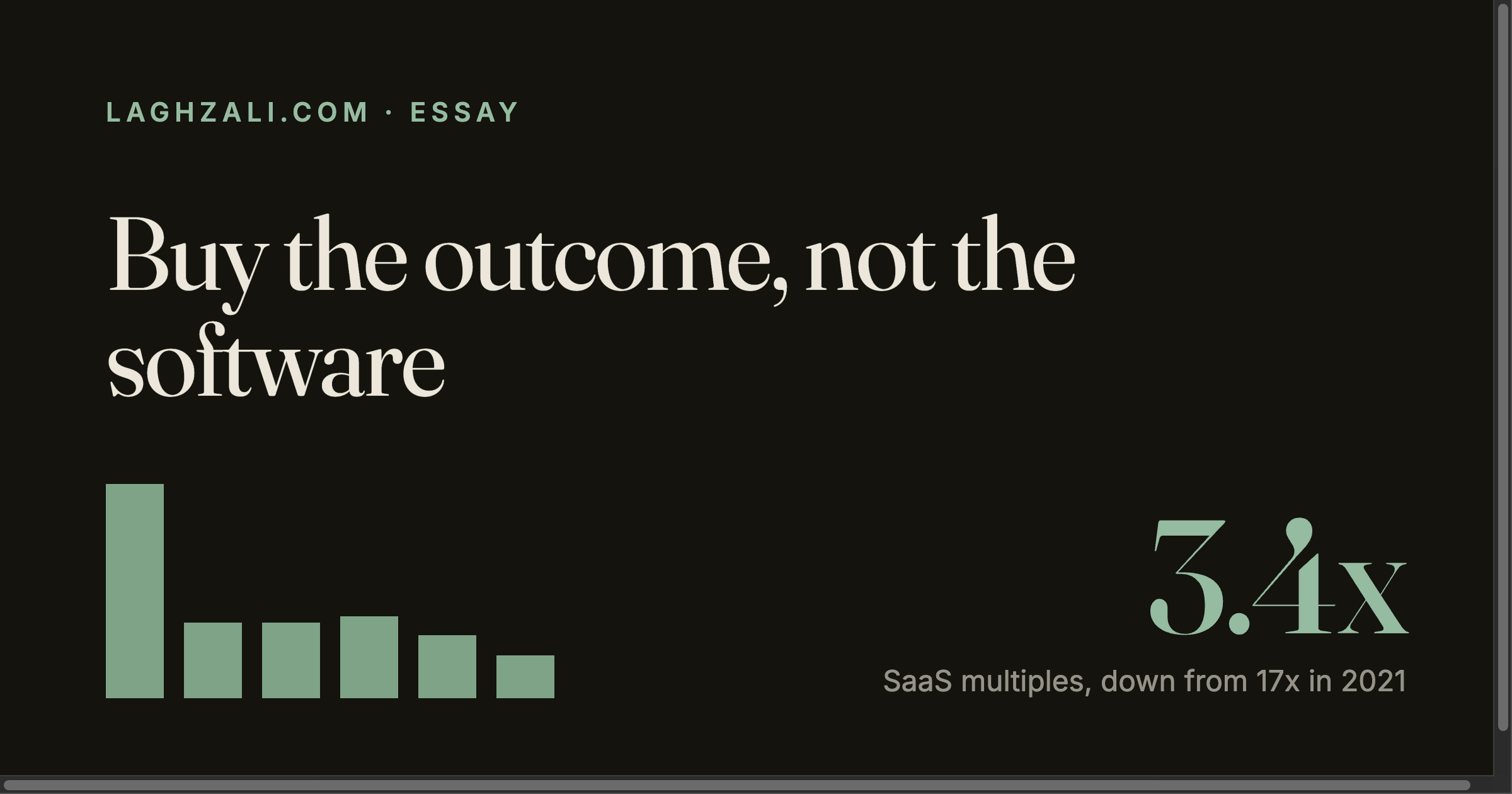

Median public SaaS EV to forward-revenue multiple. 2021 shown at the midpoint of the 16 to 19x peak range. Source: Aventis Advisors, March 2026.

Public markets are not waiting for your opinion. The median public SaaS company traded at roughly 17 times forward revenue at the 2021 peak. By March 2026 that number was 3.4.5 Call it an 80 percent haircut.

Some of that is interest rates. Most of it is colder than that: the market is starting to price the substitution. If an agent can run the workflow end to end, why would a buyer keep paying for fifty seats plus the license stacked on top? The seat is no longer the safe place it used to be.

Y Combinator’s bet

Jared Friedman, a managing director at Y Combinator, said it on the Lightcone podcast in November 2024. Vertical AI agents could be ten times bigger than the SaaS companies they replace, and roughly three hundred billion-dollar companies will be built in that one category.6 His advice to founders was blunt. Do not sell the agent to the law firm. Start the law firm, staff it with agents and put the old one out of business.7

That is the supply side of your shift. Y Combinator is funding companies whose product is the finished work, not the tool that helps someone else finish it. And it is already a wave, not a forecast. By the summer 2025 batch, 88 percent of the companies were AI-native.8

Annual revenue per employee. Midjourney: about 500M dollars across roughly 107 people. Cursor: about 3B dollars ARR across roughly 300 people. Sources: GetLatka, Anysphere, 2025 to 2026.

The economics are the part you should not look away from. Midjourney did 500 million dollars in revenue with around 107 people, bootstrapped, no outside money.9 Cursor crossed 100 million dollars in annual revenue twelve months after it started charging, the fastest any software company has ever done it, with a team you could fit in a meeting room.10 Output came unbolted from headcount. That is the thesis in one chart.

What the orchestrator does differently

I wrote here before about the move from executor to orchestrator: the edge stopped belonging to the person who does the work fastest and moved to the person who decides what gets done and judges whether it is good.

Buying is the next face of the same shift. The executor buys tools and operates them. The orchestrator skips a step: buy the result, then check it. You stop asking which software will let your team do this and start asking who will hand it to you finished and how you verify what they hand over.

It changes what you measure. Not seats deployed, not adoption, not how many of your people logged in this month. Tickets resolved. Memos drafted. Pipeline built. Code shipped. You pay for what the agent earns, not for what your team can be trained to operate.

How to buy outcomes without getting burned

A warning, because the gold rush has a tax. Bessemer’s 2026 pricing playbook flagged it: soft ROI sold fine in 2025, when everyone was buying AI at any cost. As the pilots hit renewal, the bill has to match the work actually delivered.11 Gartner expects more than 40 percent of agentic AI projects to be cancelled by the end of 2027, on cost and governance.12

So buy where the outcome can be counted. A resolved support ticket can be counted. “AI-powered synergy” cannot. A few rules I hold to:

- Pay per result, not per seat, wherever the result can actually be measured.

- Watch the metric definition. A vendor that counts a deflected chat as a resolved ticket is selling you a number, not an outcome.

- Keep a human on the output. The orchestrator judges, and that judgment does not get outsourced.

Share of enterprise applications featuring agentic AI. Source: Gartner, 2025.

The direction is not subtle. Gartner has agentic AI going from under 1 percent of enterprise applications in 2024 to 33 percent by 2028, and resolving 80 percent of standard customer-service queries on its own by 2029.13

The next thing you buy

The unit of value is changing under you. Access, out. Result, in. SaaS sold you a seat and trusted you to make it worth something, which sometimes happened and mostly did not. The agent sells you the thing the seat was supposed to produce in the first place.

For five years the work has been to become an orchestrator instead of an executor. The buy side just caught up. You spent that time learning to judge output instead of producing it, so now you get to purchase it the same way.

Go look at your last software renewal. The biggest line on it is almost certainly still priced per seat. That is the one to rethink first.

Sources

- Sarah Tavel, “AI startups: sell work, not software”, LinkedIn, August 2023. link

- a16z enterprise team, “From demos to deals: insights for building in enterprise AI”, June 2025. link

- Foundation Capital, “AI leads a service-as-software paradigm shift”, 2025. link

- a16z, “AI is driving a shift towards outcome-based pricing”, December 2024 (Zendesk per-seat example); Intercom pricing, Fin at $0.99 per resolution. a16z, Intercom

- Aventis Advisors, “SaaS valuation multiples”, March 2026. link

- Jared Friedman, Y Combinator, Lightcone podcast, “Vertical AI agents could be 10X bigger than SaaS”, November 2024. link

- Jared Friedman on full-stack AI, Y Combinator, 2025. link

- Extruct, “Y Combinator Summer 2025 batch analysis”, 2025. link

- GetLatka, “Midjourney revenue 2025”. link

- TechCrunch, “Cursor’s Anysphere nabs $9.9B valuation, soars past $500M ARR”, June 2025. link

- Bessemer Venture Partners, “The AI pricing and monetization playbook”, February 2026. link

- Gartner, “Over 40% of agentic AI projects will be cancelled by 2027”, 2025. link

- Gartner, agentic AI in 33% of enterprise apps by 2028 and 80% of customer-service queries by 2029, 2025. 2028 figure, 2029 figure